We're 60 with $2.8 million, Can We Spend $13,000 Per Month if We Retire Now

Tim explores a detailed financial review of a couple with a net worth of over $3.5 million, as they consider retiring at age 60. He covers assets, insurance, healthcare concerns, investment strategies, and tax planning to determine if they can comfortably spend $13,000 per month for the rest of their lives.

Current Situation

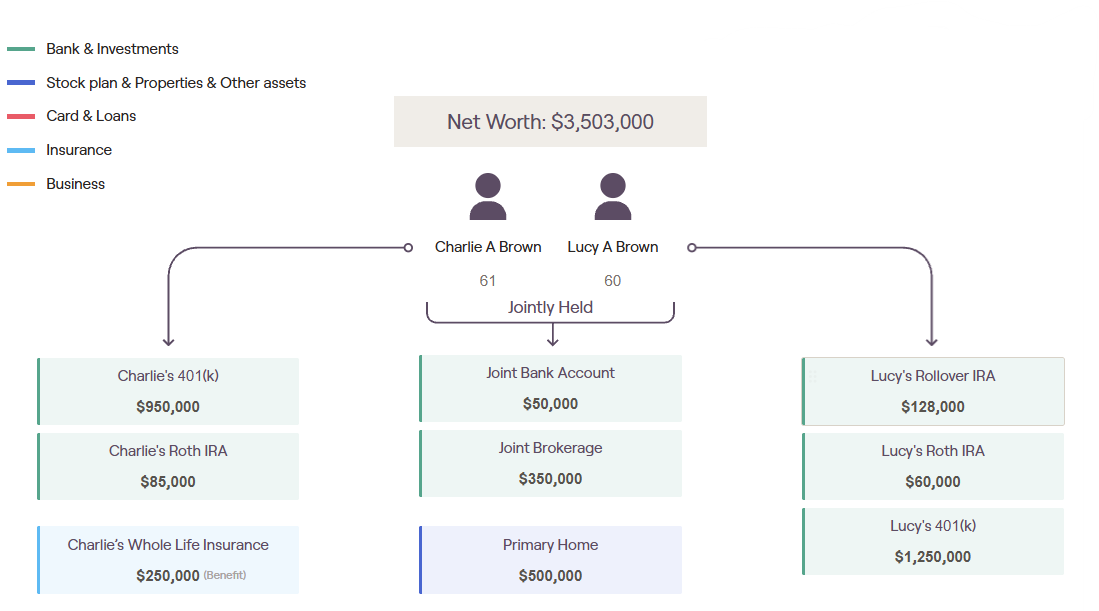

We are going to discuss Charlie and Lucy Brown, whose names frequently go through our process. See other scenarios below this post. The dates, ages, and the quantities of their investment accounts have been adjusted a bit for anonymity, but this is a real life scenario from a real couple that we've recently helped and have brought on as clients.

In this scenario, Charlie and Lucy Brown have a net worth of a little over $3.5 million. They have investable assets of $2.8 million and they are both age 60. Lucy wants to know, if we retire right now, can we spend $13,000 per month for the rest of our lives? So that is what we are going to go over today.

Blueprint

Let's start with their blueprint.

- They have over $3.5 million net worth, so they've done a great job building up an nest egg.

- Charlie has close to a million in his 401(k) and he has $85,000 in Roth assets.

- Charlie has some whole life insurance that he's not sure if they need anymore. We're going to cover an idea of what we might want to do with that because that was a question they had.

- They have some joint bank assets, some joint brokerage, primary home

- Lucy has $1.25 million in her 401(k). And then she has some Roth assets as well, and a rollover IRA.

They also have some questions about healthcare because they're only 60. They are not going to be covered by their employer until 65 like some of our clients are. Luckily, we have some answers for them.

Dashboard

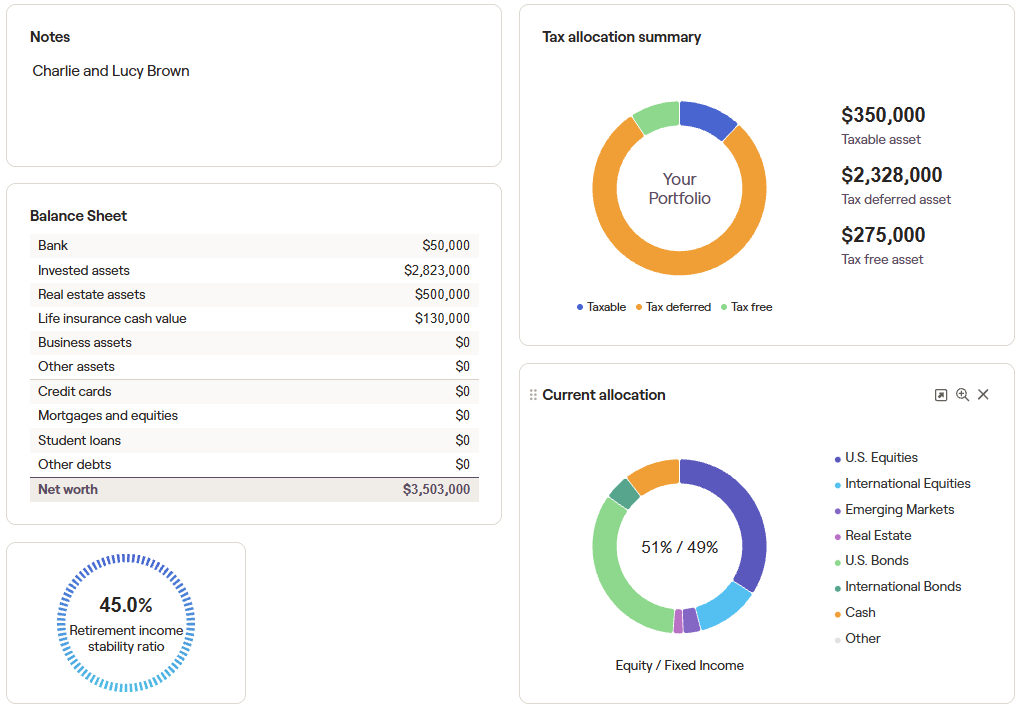

Let's click over to their dashboard to take a look at their investments and their breakdown of what they own. By looking at this, I know a few things right away. They know that they're pretty conservatively invested. They're current allocation is about 51/49% equities to fixed income.

We have not yet taken them through the investment policy statement meeting that we do with all of our clients to determine their risk tolerance and how they feel about everything, but we're going to take this from about 50/50 to about 60/40 for this demonstration to show how their assets could change over time.

Obviously, the actual situation is much different than the straight slowly increasing lines that the planning software shows. It doesn't show all the bumps and ups and downs that actually happen in real life, but it's pretty good over the long term. It's a good place to start.

We have our three account types: taxable assets, tax deferred, and then tax free, which is our Roths. So their tax deferred assets is the lion's share of what they have. This is quite standard really. That's what you've been told to do for the last 30, 40, 50 plus years, right? You work, you put your money in a 401(k), and then when it comes time to retire, then you think, how do I get this money out of there without paying Uncle Sam too much?

Well, that's why people like me have jobs. Their over $2.3 million in tax-deferred assets is going to be taxed as ordinary income for them at some point in the future. That is going to be taxed at our seven bracket ordinary income brackets, which are the highest in the code right now. So, we are definitely going to take a look at that.

They also want to know how do we turn our nest egg into an income stream without getting hosed in taxes? Well, that's another thing that we do. We definitely want to take a look at that and make sure that we're minimizing taxes for them over the course of their retirement.

Goals

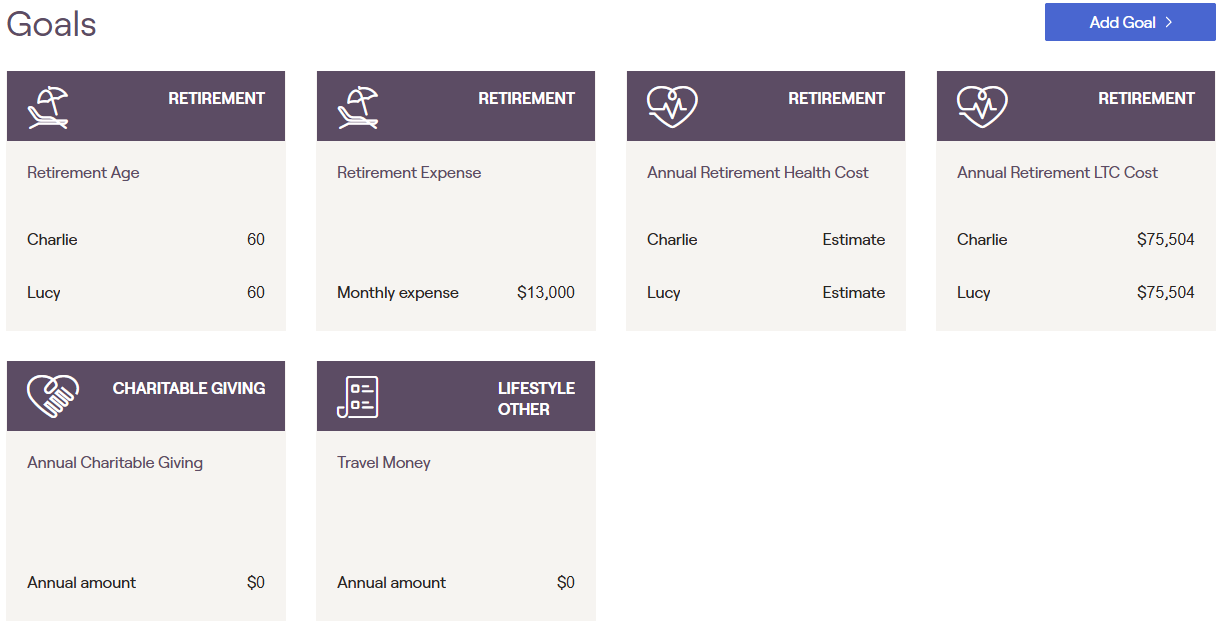

They want to be able to spend $13,000 per month, and Lucy also has an $80,000 pension that's going to kick in at age 62. Right now they're 60. Then we're also going to discuss Social Security. But these are their primary goals. They didn't say anything big about travel or trying to cover college expenses, but they figured at $13,000 per month, that would cover pretty much everything that they might want to do in a year.

Looking at Options

Probability of Success

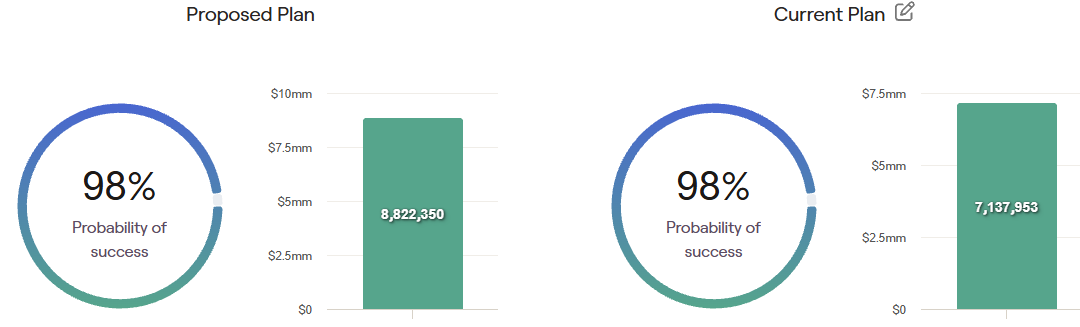

Then, of course, everything is going to be inflation adjusted for us as well. Right off the bat, if we look at their probability of success, they are at a 98 probability. Now, what does that mean? That basically means that there is a 2% chance that we're going to have to change something. Basically, if you're at 100%, that means there's 100% chance that you're underspending your retirement. At 98, you're really close to that.

This right away shows me that they have options. What I like to do is also show it in dollar terms. I've already changed this from their current allocation to moderate. So that's going to put them about 60/40 as opposed to 50/50 on their investment risk tolerance. A little bit more equity exposure should get them a little bit better returns over time. That is the difference here.

I run everybody out to age 90 when they're this young. Usually when people get to about 80 is when we start making adjustments. Usually we have a better idea of, how is your health? How are you feeling? So on and so forth. But for now, small changes now can have big impact later on as I'm sure you can imagine.

That's 30 years from age 60 to age 90. If we went a little bit more aggressive in their portfolio from 50/50 to 60/40, they're going to have a couple million dollars more at age 90. They were already thinking they probably needed to be a little bit more aggressive before they met with me.

Their probability of success is actually the same.

Social Security

A lot of times, people don't know for sure what to do when it comes to Social Security. If everybody knows exactly when they're going to die, then we know that we're always going to want to maximize the money that you're going to get from the government.

Any planning software is going to say, both wait until age 70. But what I found is when you have two people that have worked their whole career and they have a decent Social Security benefit, a lot of times they want to start getting that money sooner. So rather than having them both start at 62, what we like to do sometimes is have a bridge where we take the lower earning spouse's Social Security and flip that on.

If they both retire at 60, then we're going to flip Charlie's benefit on at 62. Then we're going to wait for Lucy's until either full retirement age (67) or age 70. For his plan, we've used age 67 for illustration.

So, we're getting a bridge. We're getting a little bit of the income in from Social Security because you paid into it your whole lives, right? You want to start getting that money back. And then we are going to wait until maybe age 70 for her, but at least full retirement age.

Then we wait and see how their assets are doing at the time. If they're comfortable and retirement's going well, if we get to full retirement age and the market goes down 50%, we might flip on Lucy's Social Security. Then if everything's going great, then we might wait until age 70 because then, if something happens to one of them, the higher benefit remains.

So, we like to do that bridge and that's what we've planned here for Charlie and Lucy because they had mentioned that they wanted to start getting Social Security, but they also understood doing smart planning as well.

For this illustration we have used age 62 for Charlie and then we have used age 67 for Lucy on when to time Social Security.

Cash Flows

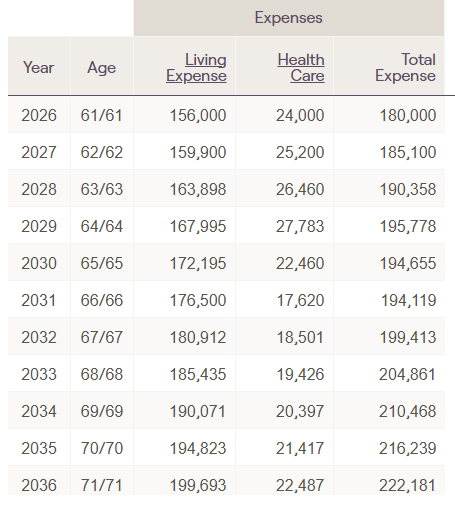

Now let's take a look at all of the cash flows that are going to be affecting them, inflows and outflows, or income and expenses. They want $13,000 per month in retirement. That's their living expenses. And then there's healthcare. They're going to be 60, so they can't get Medicare quite yet, so their healthcare could be expensive.

Healthcare

We work with a firm called MoveHealth, and they help coordinate Affordable Care Act (ACA) credits for people in this exact situation, making sure they're keeping income at certain levels so that they can get credits toward their healthcare.

Their healthcare might not actually be $24,000 per year, but I left that in here just to hedge and be a little bit higher than normal, but we've seen cases like this where we've gotten it from $24,000 per year for a married couple before age 65 down to $1,000. So this is a big part of planning.

That is a huge difference between ages 60 and 65. You've got four or five years where you have to pay for healthcare. That's about $100,000 in savings over 4-5 years. We've partnered with a company that helps with that, so that's what we're going to do for Charlie and Lucy.

For illustrative purposes here, we have their healthcare up until age 65. Then Medicare kicks in at age 65 and they start paying their Parts B and D premium.

Back to their expenses. So, they have living expenses and healthcare. Those are their two primary big expenses. The living expenses are going to be after tax, but they're going to cover everything that they need to do. That's based on the numbers that they gave me and that's what we went with just to keep it short and sweet.

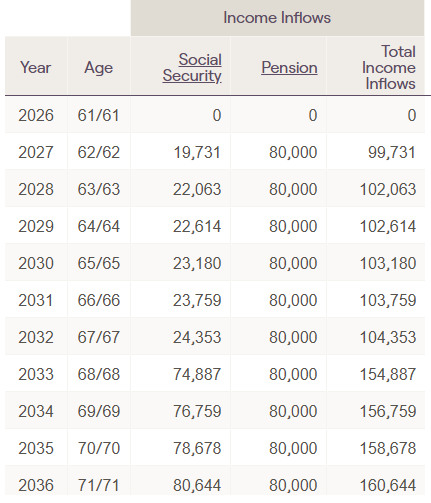

Income Inflows

Then I did the income inflows as if they will retire tomorrow. Charlie's Social Security and Lucy's pension do not kick on until age 62, so we are starting retirement with zero Social Security and zero pension.

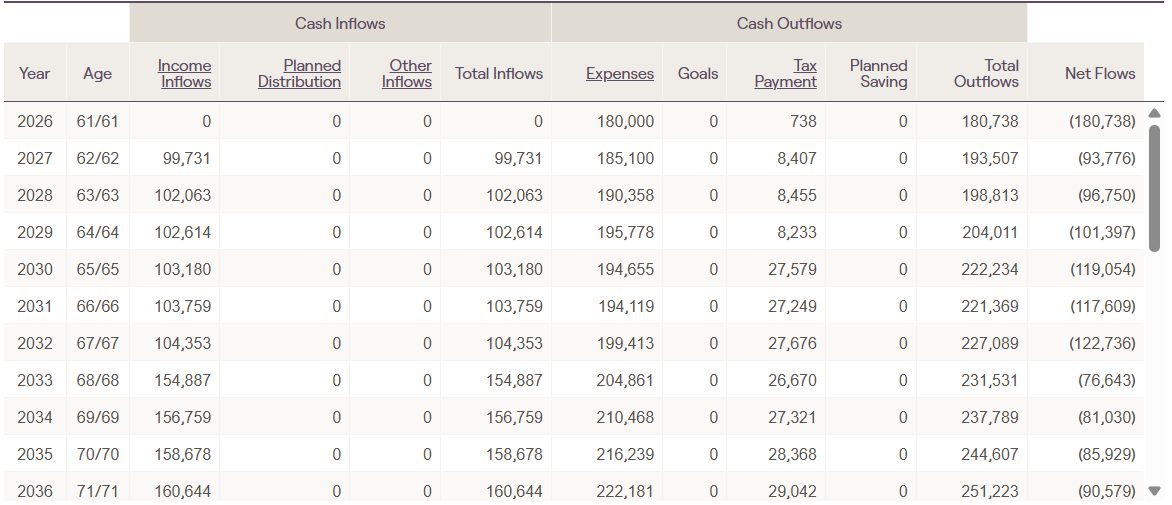

Looking at net flows, the amount needed to live off of would have to come out of their assets. The software automatically says, if we don't have any income, then we have to take it out of the portfolio. That net flow is big the first year, then it goes down, then it stays about the same.

These are inflation adjusted 2.5%. We know we're going to have inflation. We don't know exactly what it's going to be, but I think 2.5% inflation over time is probably generally going to be pretty good.

Then it bumps up a little bit, but then once we get to age 68, Lucy's full Social Security kicks on as well. That's why they have a big income inflow there. Then the net flows needed from their portfolio go down.

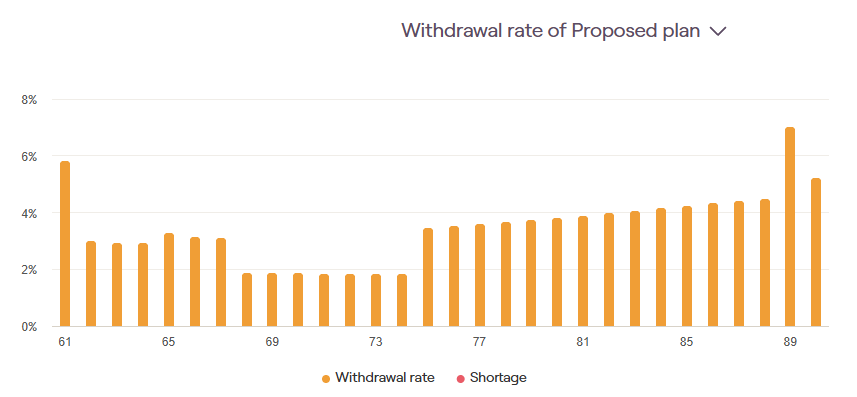

Withdrawal Rate

Now that we've looked at the net flows and how that's coming out of their portfolio, let's take a look at their withdrawal rate and make sure it's sustainable. As we already saw, they have a 98% probability of success. Their plan says right now that at age 90 they have a high probability that they would have $1 million in their portfolio. So we know just from that they're in good shape.

If you have a few years with over 6% withdrawal rate, that's fine but generally throughout retirement if we can keep it between 5% and 6%, that's pretty much the sweet spot. We're obviously going to make adjustments. I know the standard 4% rule is probably what a lot of you have heard about or are familiar with.

We use guardrails with our investment process. We adapt to the market. This very first year, we're approaching 6%, but we don't even hit it for them. Even that very first year when they have to take out the most because they don't have their pension or Social Security income yet, we're not even getting to 6%. And this is just one year, so they are in great shape.

So we go from under a 6% withdrawal rate and then down to under 3% and then down to under 2% when both Social Securities kick in. Then at age 75 they have to start taking their RMDs. That's why the withdrawal rate gets a little bit higher, because they're forced to withdraw that money.

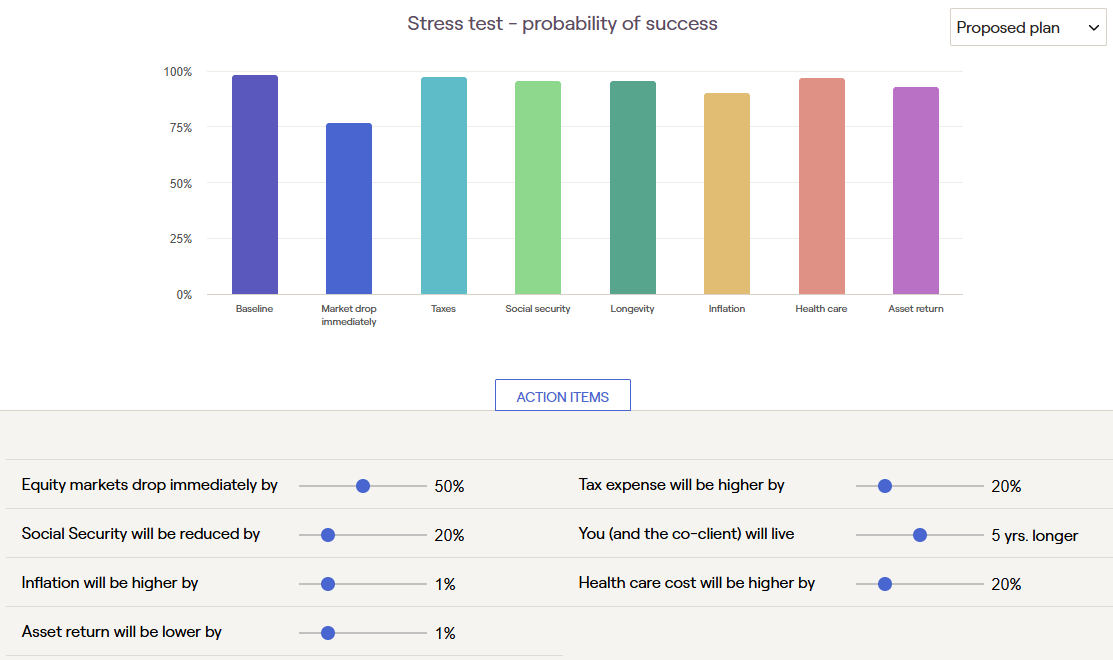

Stress Test

I also like to do a little bit of a stress test. Let's say the stock market drops by 50%. What's the probability of success success going to be for them then?

It's still going to be 77.6%. This just basically means that we're going to have a 23% chance that we're going to have to make some changes. I would be completely comfortable with this.

If any of our clients are between 60 and 100% probability of success, that's great. That just means we're going to have to make changes, but we're going to have to change things as soon as you walk out the door anyway, right?

So, even with a 50% market drop, they are still in great shape.

Now we know the stress test and we know that they can spend $13,000 a month. The answer to Lucy's question is, yes, you can retire now and spend $13,000 a month. And Armageddon aside, it should last throughout your retirement pretty easily.

So, let's say we take that $13,000 a month and we raise it up to $16,000 per month. What does that do? Now, they're still at a 75% probability of success. Again, that's really good. That just means there's a 25% chance we're going to have to make changes, and we're going to make changes anyway, right?

But this means that they are still spending and they still have adequate income and expenses throughout the course of their 30 plus year retirement.

Let's see what that looks like as a dollar amount. Instead of saying, we're going to make it to age 90 with just under $10 million, now we're going to have just under $7 million. So, still looking very good for them even with spending $36,000 more per year.

So, again, I just like to show everyone where they're at. It's not perfect, but it helps people get a good plan and a good starting point of their scenario.

Tax Strategies

On to tax strategies and tax savings. They have over $2.3 million of their nest egg in tax deferred accounts. We need to help them thread that needle and optimize and lower their lifetime tax liability.

Asset Location

The big ways we're going to be able to do that are what they call equity allocation, which is asset location, which basically means making sure you're putting the right investments in the right accounts over time. Because if you're going to have an asset go from 10 to 100 over time, you're going to want that in a Roth or tax free account.

Next, you would want that growth in a taxable account because once we get the long-term capital gains and qualified dividends tax rate, those rates are much preferred to our ordinary income tax rates.

Then any of the fixed income or stuff that's going to pay out a steady dividend or interest over time but probably isn't going to grow as much, we want that in the tax deferred account because we're going to get taxed on those withdrawals at the seven bracket ordinary income tax rate.

Sequence of Withdrawal

People often don't always realize this, but the sequence of withdrawal of where you take the money from when you retire can have a very big tax effect over time.

A lot of times people think, I've got three different account types (taxable, tax free, and tax deferred). I need $150,000 a year. I'm just going to take $50,000 from each account every year. That's not the best way to do it.

Generally, you want to start with a taxable account and then you want to go through your tax deferred and then leave the Roth for last.

If you thread this needle now, every year, it's not going to be exactly the same each year. That's why it's always best, in my opinion, to walk with someone like me that's going to help you thread that needle every year. You might want to fill up certain thresholds.

You might have hit a threshold and you think, I don't want to go over this threshold. There's no reason for us to be in the 32% or 35% tax bracket, or whatever it might be.

So you want to make sure that you're paying attention and taking money from the right account in your retirement, because in retirement, where you get the money from for expenditures has a bigger effect on your tax rate than your actual income. So we always want to be cognizant of that.

Roth Conversions

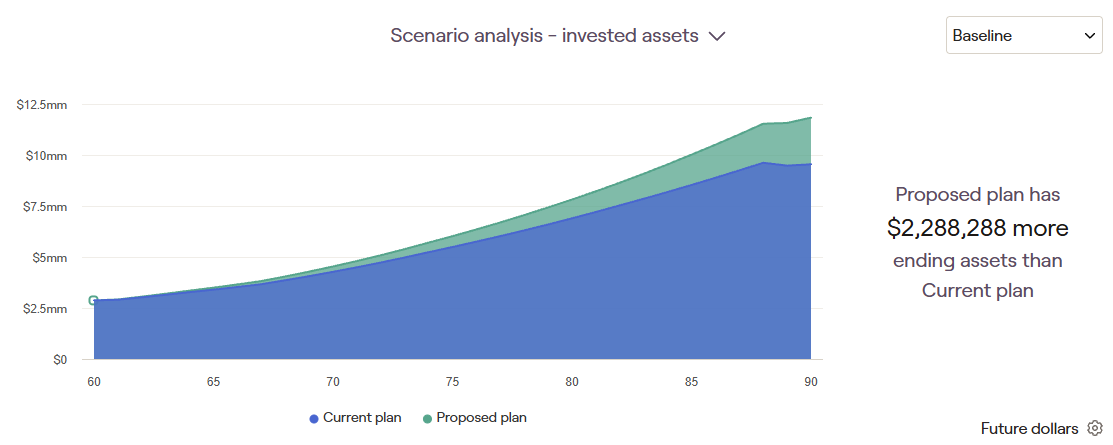

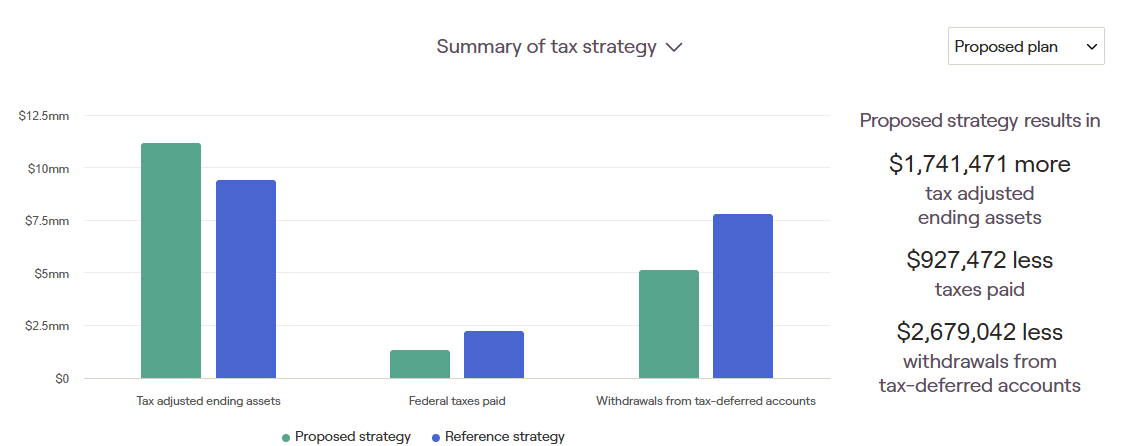

Then, of course, we do Roth conversions. A Roth conversion is taking some of those tax deferred assets and filling up certain thresholds over time to minimize and lower lifetime tax liabilities. Charlie and Lucy Brown are in the 22% tax bracket. Over a 30+ year retirement, Roth conversions will save them about a million dollars in taxes.

Now, saving money on taxes is great, right? But it doesn't really do any good if we don't have more assets. We're going to have over $1.7 million more in tax adjusted ending assets for Charlie and Lucy.

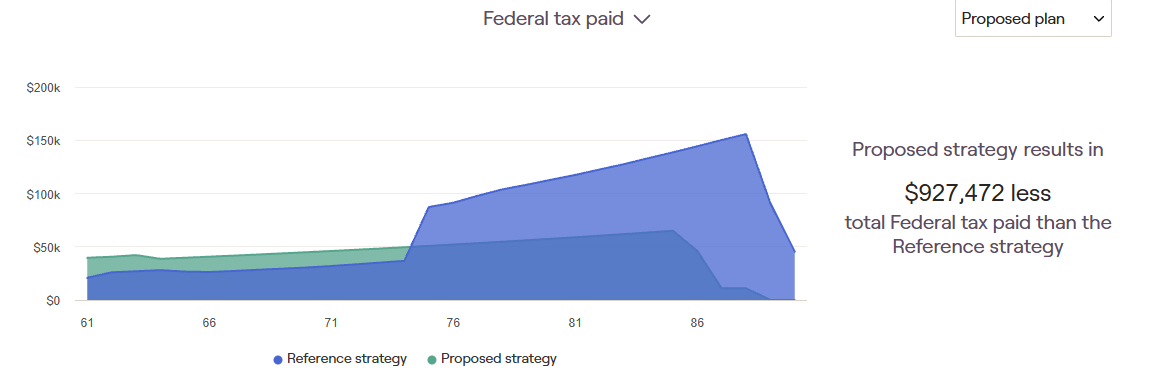

For a visual of those tax savings, if we do nothing and they just keep letting their tax deferred accounts grow and then they have to start taking their RMDs at age 75, they're going to have a big spike in income because their tax deferred accounts have grown and now they have to start taking RMDs.

So now, not only are they going to pay a higher tax rate than they needed to because they haven't been doing Roth conversions, but it's also going to affect their Medicare Parts B and D premium because those are based on your adjusted gross income.

Once you start tripping those IRMAA Medicare thresholds, the stair steps get closer together. So it's easy for you to hit that first threshold with an RMD and Social Security and pension, and then maybe next thing you know, you're up to the third or fourth threshold and you're paying an extra $8,000 to $10,000 a year in parts B and D premiums. So, we definitely want to be cognizant of that.

Another reason why Roth conversions help alleviate that later on in retirement, even if for a few years we do Roth conversions big enough to go into some of those brackets, we're doing it intentionally to lower and flatten the total amount of taxes paid.

If we do nothing, this is our tax situation with the Roth conversions. This is the amount of less tax that they'll pay. See, we've gotten rid of all of this light blue here. And these are the kinds of things that we're going to be able to do for them to help them minimize and optimize their taxable situation and definitely get their lifetime tax liabilities to the lowest possible rate because we want to pay Uncle Sam every penny that we owe, but not one penny more. Right?

Whole Life Insurance

I mentioned at the beginning that they had a whole life policy with some cash value. Sometimes we want to keep a whole life policy for estate planning, but right now the lifetime estate tax is really high. It's over $15 million, and $30 million if you're married. In Illinois, it's only $4 million. They live in Illinois where we're based. So once you start approaching $4 million, if you're married, you'll probably want to talk to an estate attorney about splitting the assets into a trust. So that'll get you up to 8 million total.

But for now, we're not going to worry about that. We're going to say, we've been putting money in this policy. We have cash value. I don't feel like we need the insurance anymore.

The death benefit is $250,000, and that's not even 10% of their net worth. Plus, when they got this policy, things were a lot different. They didn't have the assets. They had debt. That's what insurance is for, right?

If we take that cash value out, that's going to create a huge taxable event for them. But they are concerned about health and they're concerned about long-term care. So we're going to look at a 1035 exchange, or doing a non-taxable transfer from the whole life policy into a different type of product that will, at the very least, have a long-term care rider.

Then if something happens to Charlie, he's going to be covered with long-term care if he needs it, by taking that $130,000 in cash value and basically turning it into a product that will still have a death benefit.

That was another question that we answered for them. That's the kind of stuff that we do every day when we're helping people retire and they come in with assets that they've had and been putting money into for the last 30, 40, 50 plus years of their lives.

So, the answer to Lucy's question is yes, they can spend more than $13,000 per month if they retire now and for the rest of their retirements. They are in great shape.

Every household's a little bit different, but the concepts that I use are going to be applied the same way. It's always a function of numbers and also talking to get a feel for where people are.

Going Further

If you are interested in seeing other case studies, check out the videos in these posts:

- We Have $3.5 million, Can We Retire and Maintain Our Lifestyle?

- I have $2 Million, I'm 56, and I Want to Retire Now

- Can We Spend $10,000 per Month in Retirement?

- We have a $2.4 Million Portfolio; Can I Retire Tomorrow and Continue Our Same Lifestyle?

- How Much Can We Spend if We Retire Tomorrow?

- How Much Can I Save in Taxes with Roth Conversions?

- How Much Can I Spend in Retirement from a $1 Million Portfolio?

- Is $1 Million Enough to Retire at 65?

- Real Life Case Study Saving Over $1.7m in Retirement Taxes

A CERTIFIED financial planner™ professional can help you plan for your retirement. Schedule a call today so we can talk about your situation.