We Have $3.5 million, Can We Retire and Maintain Our Lifestyle?

What if you had built a $3.5 million nest egg, owned your home outright, and still wondered: Can we really afford to retire at 60 and keep living the life we want?

In this episode, Tim puts that exact question to the test for a couple (names changed for privacy). With goals like funding weddings for their daughters, traveling while they’re still young, and keeping up their lifestyle, Tim shows how the right planning can turn uncertainty into confidence.

Current Situation

Today we're going to take a look at Aaron and Kelly Miller, whose names have obviously been changed. Right now, Aaron is 58 and Kelly is 55. They want to know if they can retire at 60 and maintain their lifestyle, and they have a few other goals that they want to hit.

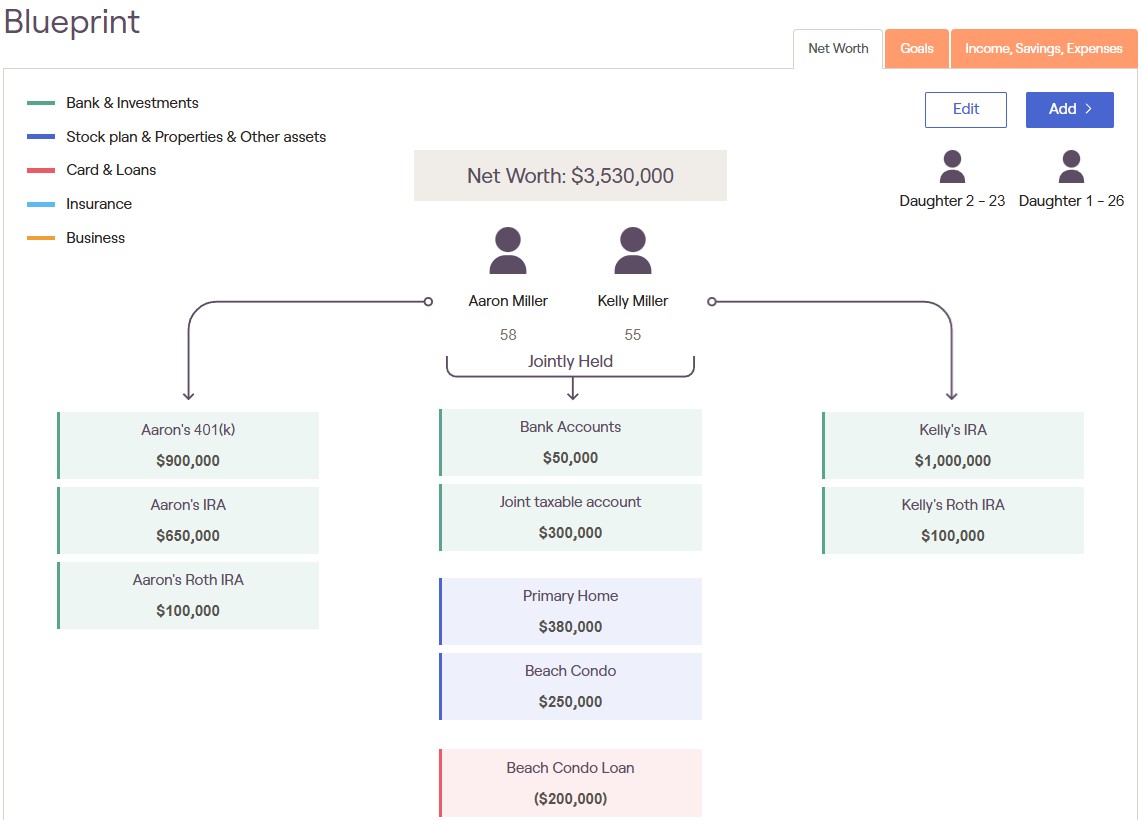

Blueprint

First we're going to take a look at the Millers' blueprint, which says they have a a net worth of over $3.5 million. So, they've done a great job building up a nest egg.

- They have two daughters that are phasing out of college right now. The oldest one is already out and the youngest one is phasing out.

- They want to include $20,000 for wedding expenses for each daughter, and we're going to assume those happen at age 30 for now because nothing's on the radar at the moment.

- They have a 401(k), IRAs, Roth IRAs, and joint accounts.

- They have a primary home that is paid for.

- They have a beach condo with a $200,000 mortgage.

They want to retire at 60 and maintain their lifestyle.

Right now, they're spending about 10,000 per month. And they say that when they retire, they're pretty sure that they will be able to keep the same lifestyle spending $8,000 per month.

They also want to be able to travel because they will be relatively young when they actually do retire at 60.

Let's take a look at their scenario.

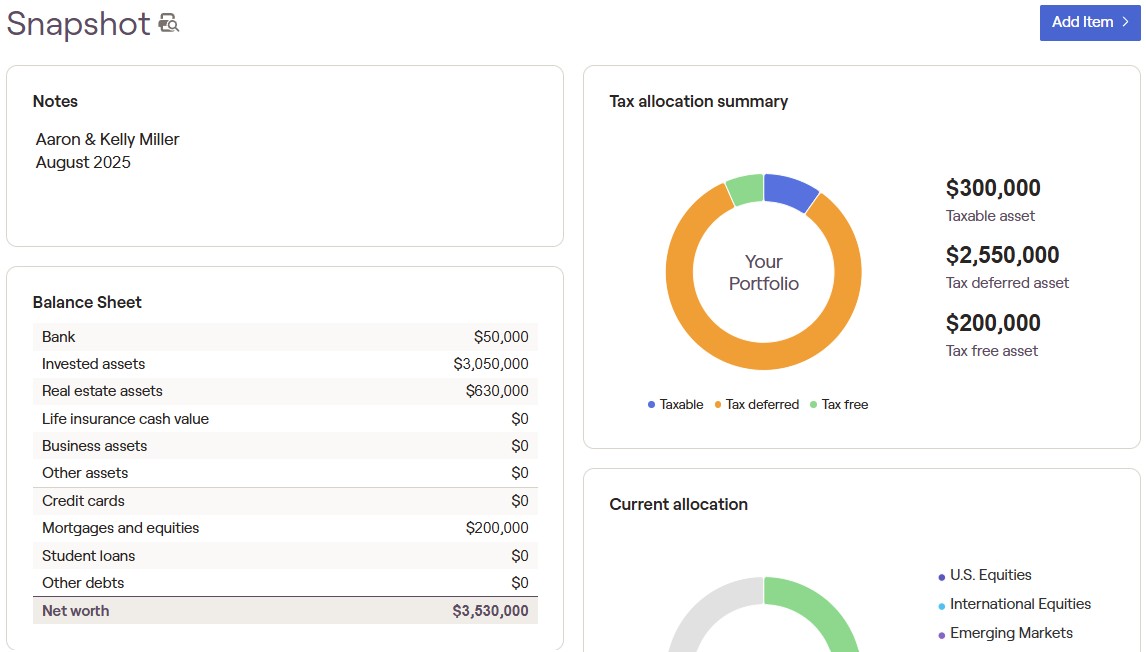

Snapshot

Here is a quick snapshot of what they've got. They do have a rather large tax deferred asset. They've done a great job, but you do always want to remember that we'll have to do a little bit of tax planning here because at some point in their future, $2.5 million is going to be taxed at the ordinary seven bracket rates. So they do definitely need to be mindful that Uncle Sam does own a portion of those tax deferred assets.

They have taxable assets of $300,000, which is great. Then they also have good start on Roths with $200,000 in their Roth IRAs, or tax-free accounts.

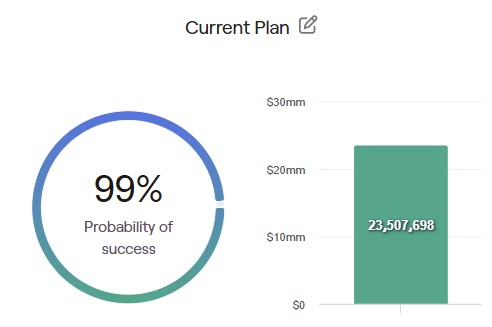

Probability of Success

So if we take a look at their retirement situation, they are in very good shape on their expected goals and spending. This includes the $20,000 for the daughters' weddings, and it includes their expected expenditures, but it does not include the travel yet.

These projections go out to age 90. So this is a ways out in the future, but this is how we start. Then as people age throughout retirement, we can start narrowing things down if and when health starts to become an issue.

They're starting with a few million dollars now but then a little over 30 years from now their nest egg is going to be about $32 million. That assumes about a 7.5% return over time in their nest egg.

So they are in great shape, but let's make a few changes.

Looking at Options

This scenario is for this specific couple, but the same principles and the same guidelines that we use can be applied to anybody's situation. Obviously, the numbers and the thresholds that are going to apply to your specific situation are going to be different, but the same principles apply.

A lot of times people come to us and they're like, Tim, are we in good shape? Can we do this? Can we do that? Well, as you can see, these guys are in great shape.

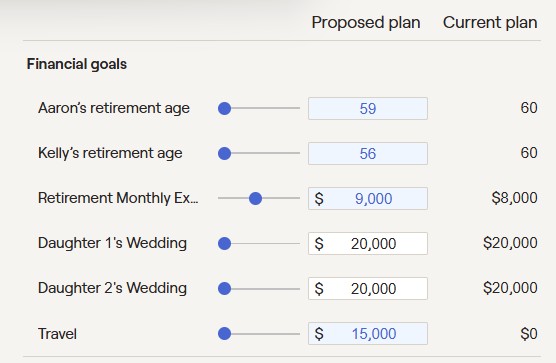

So, what if we say, hey, Aaron, instead of waiting until 60, what if you retire next year? And then Kelly, rather than waiting until age 60, what if you also retire at the same time, but that'll be four years earlier for her, because she's three years younger than Aaron.

Now, on top of that, I put a category of travel. They had estimated $10,000 or $12,000 a year, but what if they spent $15,000 a year on travel for a 13-year time frame from retirement to age 70.

Obviously, as they approach that age, if we need to make adjustments, we will. Because once people walk out the door, things start to change!

That is why we believe we add the most value when we walk with clients through retirement because every single year there's going to be different things that come up that we have to adapt to and lay the tax code on top of and make sure that we're being as tax efficient as we can.

So we have lowered their retirement ages and we have put in $15,000 a year in travel expenses for 13 years.

And now I also said, at $8,000 a month, you guys can live and do what you want. They have their beach condo mortgage at 6% interest. They have options there. They've got $300,000 in cash, so they could pay that off. It's up to them.

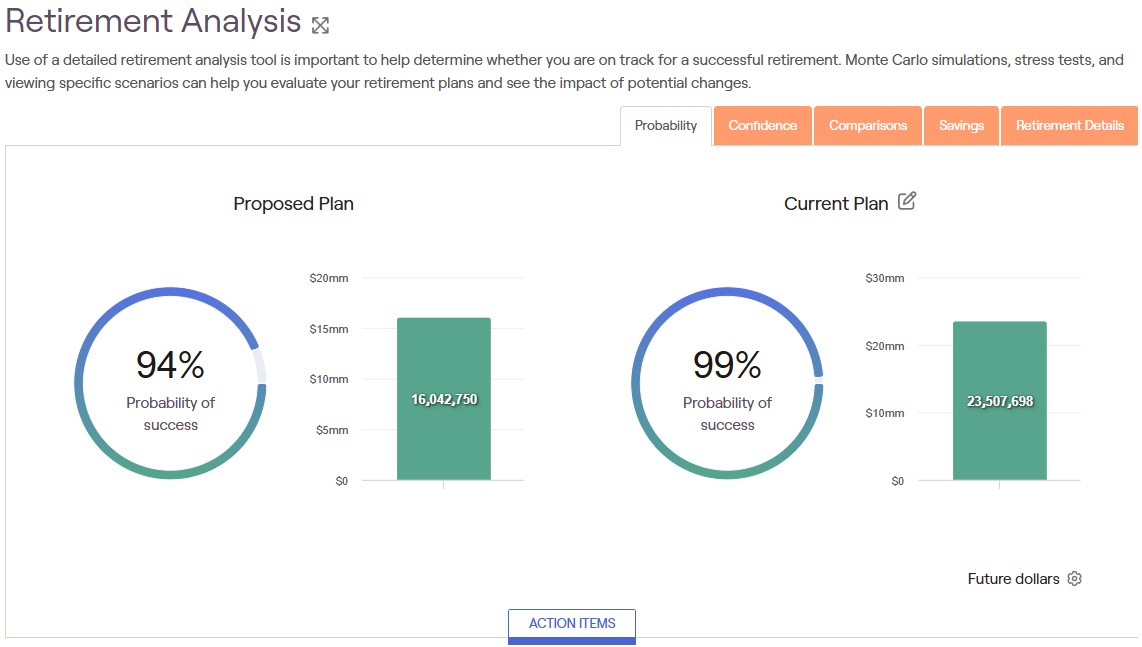

But what if we can take that $8,000 a month and raise that to $9,000 just for illustrative purposes, even with retiring a few years sooner than we thought? With those changes, we have a 94% probability of success.

That means that there's a 6% chance that we're going to have to make some changes, which is pretty low still.

I don't want you to get hung up on the numbers. These Monte Carlo simulations are great, but they can get confusing. People think, if I'm not at 100%, does that mean my retirement is going to fail? Not at all. People can be at 50% and we start making changes, and small changes now can lead to big changes later, and that gets them from 50% up to maybe 70 or 80%.

On the flip side, if you're at 100%, that basically means there's 100% chance that you're probably not going to spend enough in your retirement. And sometimes people do that. They're comfortable. They're living the way they want to live. They just had a successful career of building assets.

The biggest thing is people come to us and are like, "Hey, what can we do? What options do we have out there?"

So, that's what I've just done for these guys, Aaron and Kelly. As you can see now, it is saying with all those changes we made:

- adding the additional travel

- adding $1,000 per month for expenses in retirement

- reducing their retirement ages

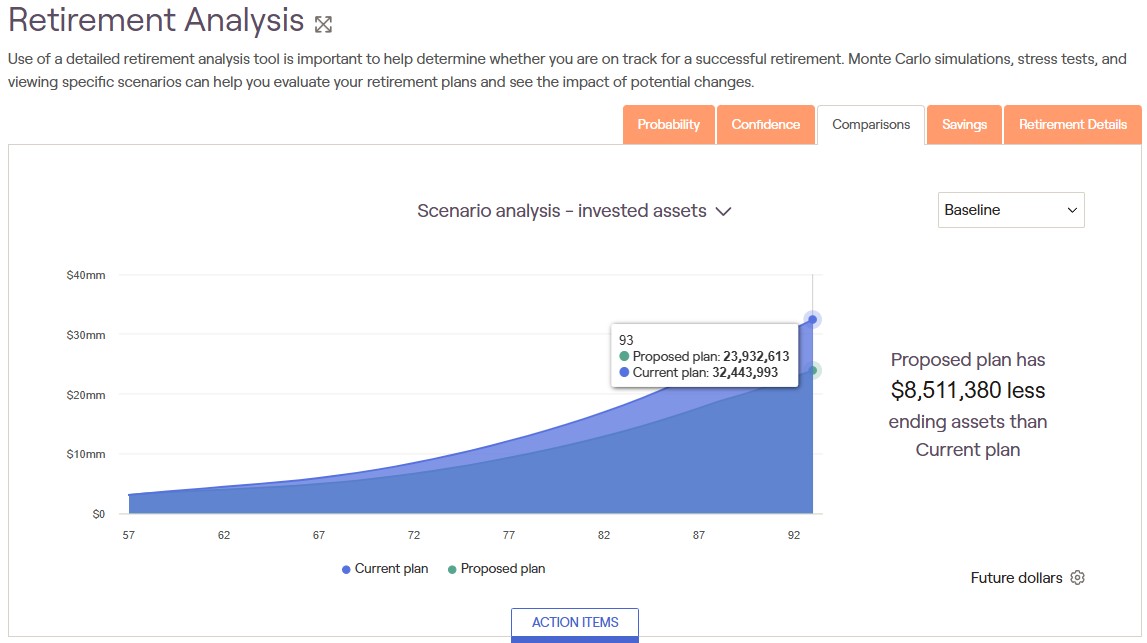

They're going to have about $8.5 million less at age 90 (Kelly's age 90 because she's younger).

The proposed plan is still going to have about $24 million at the end. So, pretty dang good, right? And again, this is 30 plus years down the road. That's why these numbers get so high. These are inflation and investment return adjusted.

Summary of Cash Flows

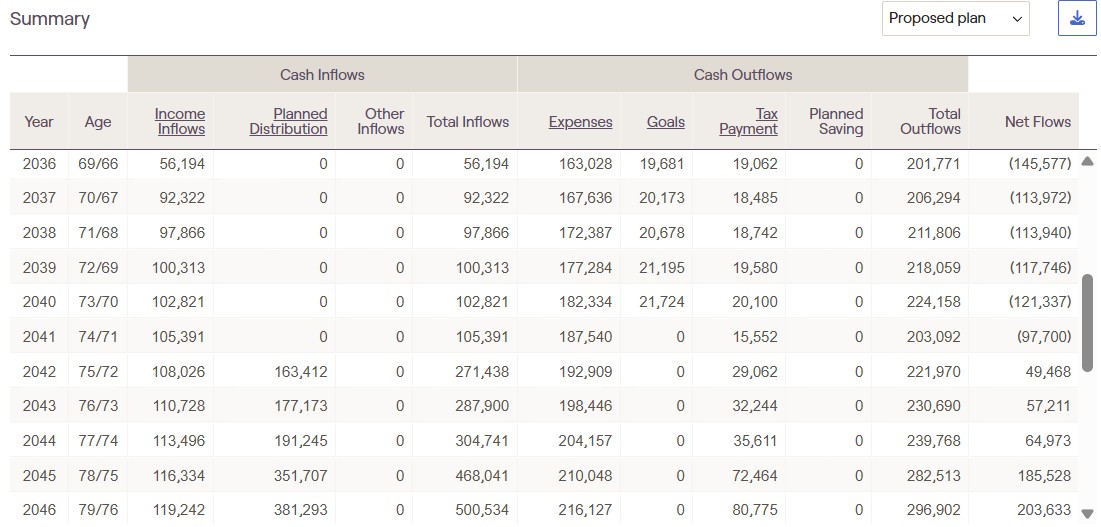

Now, let's just take a quick look at their cash flows. This is with the proposed changes that I'm going to recommend for them. As you can see, they still have a very high probability of success and a decent chunk of assets even if they do make all these changes and live to age 90.

The income inflows are assuming they work one last year.

We have expenses starting at $120,000 (because they are currently spending $10,000/month pre-retirement). Then the 2nd year includes $9,000/month in expenses plus annual healthcare costs of $13,434. Each year the numbers are inflation adjusted.

We're going to start pulling from their accounts to live off of and then we're going to have a little dip when we assume their Social Security is going to flip on at full retirement age 67 and age 70. So that's why we're not taking quite as much out of the accounts.

Then at RMD age 75, required minimum distributions are coming out so it's not pulling in money to live. That's a payment that you have to do something with because you have to start taking the RMD. And that goes back to the tax planning.

We always need to pay attention to our income down the line because of Medicare Parts of B and D premiums that might be affected by higher income down the road. Right now, one of the biggest things to remember if we're going to do Roth conversions or things like that is that tax rates right now, our seven bracket ordinary income rates, are historically low. They're as low as they have been in a hundred years, and our debts and deficits in this country are very high and getting higher, right?

The Tax Cuts and Jobs Act (TCJA) was extended and those tax cuts were made permanent, which is great for tax planning right now, but at some point we're going to have to pay the piper, right? Whether it's 5 years from now, 10 years from now, or the bond market forces some change, but that's a whole other conversation.

Back to cash flows here. Let's look at their goals.

The weddings at that time, if I assume age 30 for both daughters, we see about $22,000 in 2029 for Daughter 1 and almost $24,000 in 2032 for Daughter 2.

The travel goal of $15,000 would be about $15,800 if we had that kick on at age 60. Then we have 13 years of travel expenses. I could have started that at age 58. They're still in great shape even with these extra expenditures because they built up a great nest egg.

Withdrawal Rate

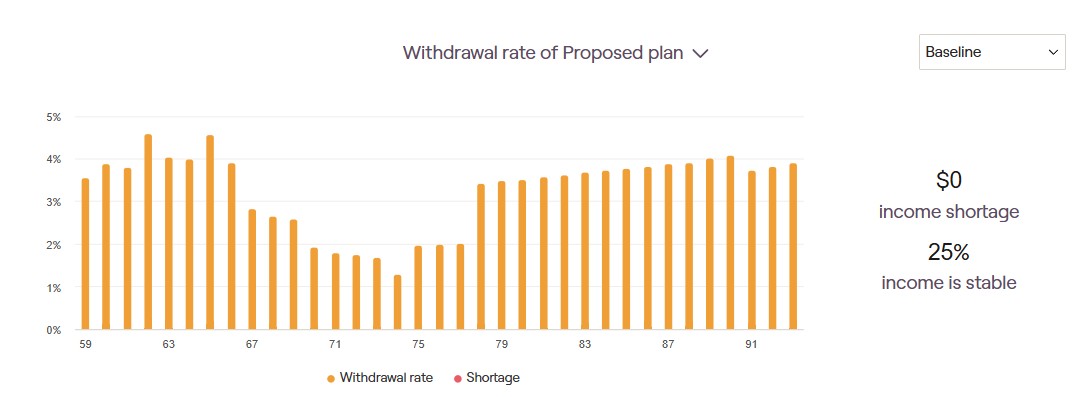

Let's take a quick look at their withdrawal rate. Now, even with these added expenditures and retiring a little bit early, they're still going to be in great shape as you probably could have guessed by their high probability of success and large amount of assets predicted at the end of plan.

These are all very doable withdrawal rates. Once Social Security kicks in, the rate goes down to 1 to 2%. The highest they get is about 4.5%. So they're not even in the 5% range. We can usually make stuff work for 30 plus years in the 5 to 6% withdrawal range pretty easily. So their withdrawal rates looks good.

If you would like to have an illustration for your specific situation, please click the button below to schedule a call and we'd be happy to take you through our process.

Going Further

If you are interested in seeing other case studies, check out the videos in these posts:

- I have $2 Million, I'm 56, and I Want to Retire Now

- Can We Spend $10,000 per Month in Retirement?

- We have a $2.4 Million Portfolio; Can I Retire Tomorrow and Continue Our Same Lifestyle?

- How Much Can We Spend if We Retire Tomorrow?

- How Much Can I Save in Taxes with Roth Conversions?

- How Much Can I Spend in Retirement from a $1 Million Portfolio?

- Is $1 Million Enough to Retire at 65?

- Real Life Case Study Saving Over $1.7m in Retirement Taxes

A CERTIFIED financial planner™ professional can help you plan for your retirement. Schedule a call today so we can talk about your situation.