I have $2 Million, I'm 56, and I Want to Retire Now

Tim dives into a real-world retirement planning scenario for a single professional with over $2 million in investable assets at age 56. He explores whether she can retire now while maintaining her current lifestyle, accounting for her assets, spending habits, and college expenses for her children.

“I have over 2 million dollars, I’m 56, and I’m ready to be done with my job. Can I retire now and spend the same amount?"

We're going to answer a question from a potential prospect we'll call Monica Geller. Names and amounts have been adjusted a bit to allow for anonymity, but today we're going to discuss her situation where she has over $2 million in investable assets, she's 56, and she wants to know if she can retire now.

Monica's Situation

Monica is single. She's spending about $8,000 per month right now. She wants to know if she can retire today at age 56 and maintain that same amount of spending in her retirement.

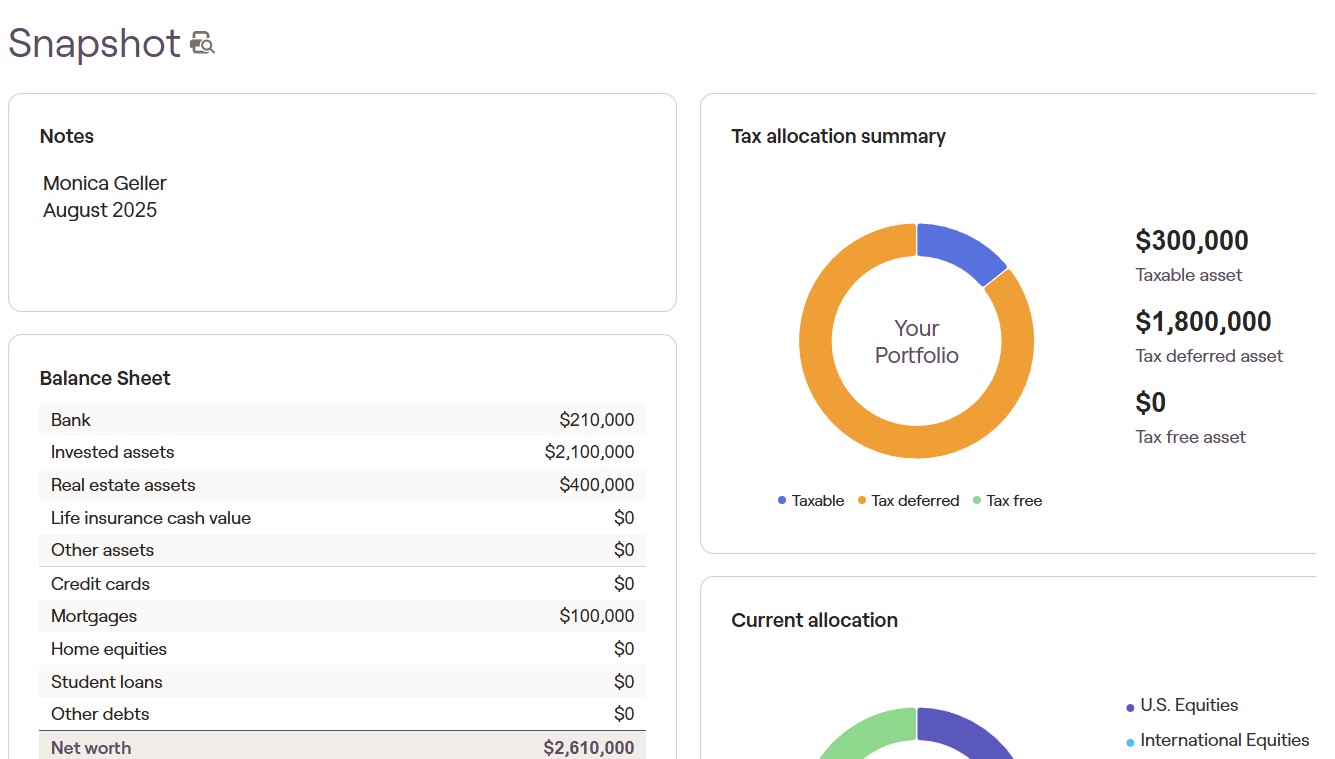

Snapshot

First, I can tell real quick just by looking at her snapshot, she's obviously done a great job. She has some bank CDs and a checking account. She has investable assets of $2.1 million, some real estate, and a little bit of a mortgage, but with a very low interest rate under 3%. So, we're not super worried about that.

Then I can see that she has a large tax deferred asset with $1.8 million that she's going to pay tax on at some point in her future. Sometimes we call that a "tax bomb" because it can really add to lifetime tax liability if not managed properly.

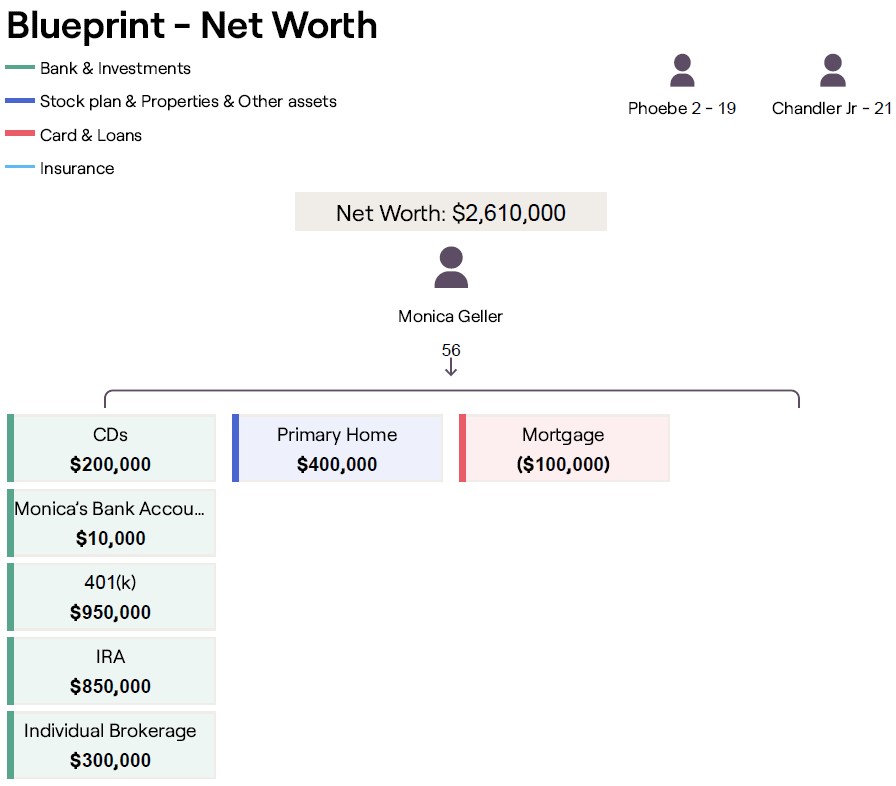

Blueprint

Let's take a look look at Monica's blueprint:

- She has two kids, Phoebe 2 and Chandler Jr., and they are both in college.

- She has a primary home with a mortgage.

- She has bank CDs, bank account, about $950,000 in her 401(k), $850,000 in an IRA, and $300,000 in an individual brokerage account.

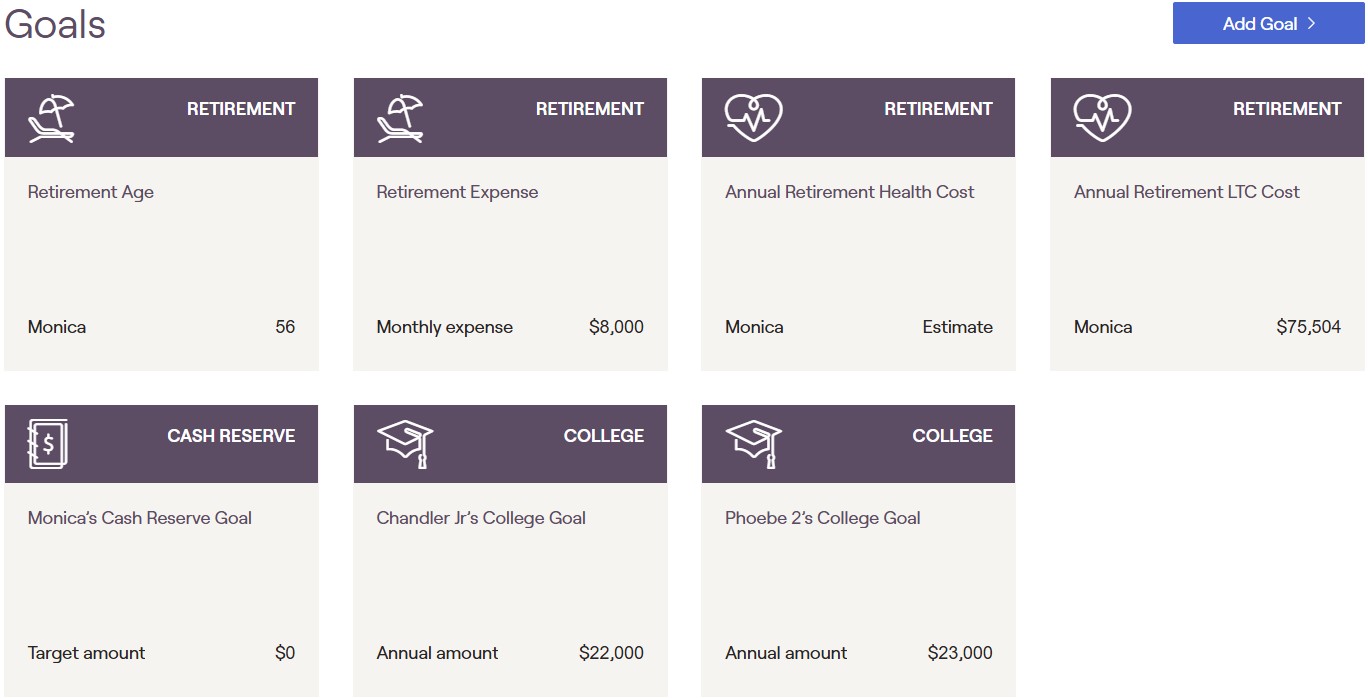

Goals

Let's look at her goals:

- She wants to retire now, at age 56.

- Her retirement expenses are going to be the same as what they are today, which is about $8,000 per month.

- She is expecting to spend about $100,000 in college expenses for Chandler Jr. and Phoebe 2 to get them through and out the door and on their own (hopefully, right?).

If she retires today, she is still going to have these expenses, and she's not going to have any more income, at least not until we flip on Social Security. We have put Social Security in at full retirement age, which for her is going to be age 67, so 11 years from now. She is going to be living on her assets until that time. Let's take a look at what that means.

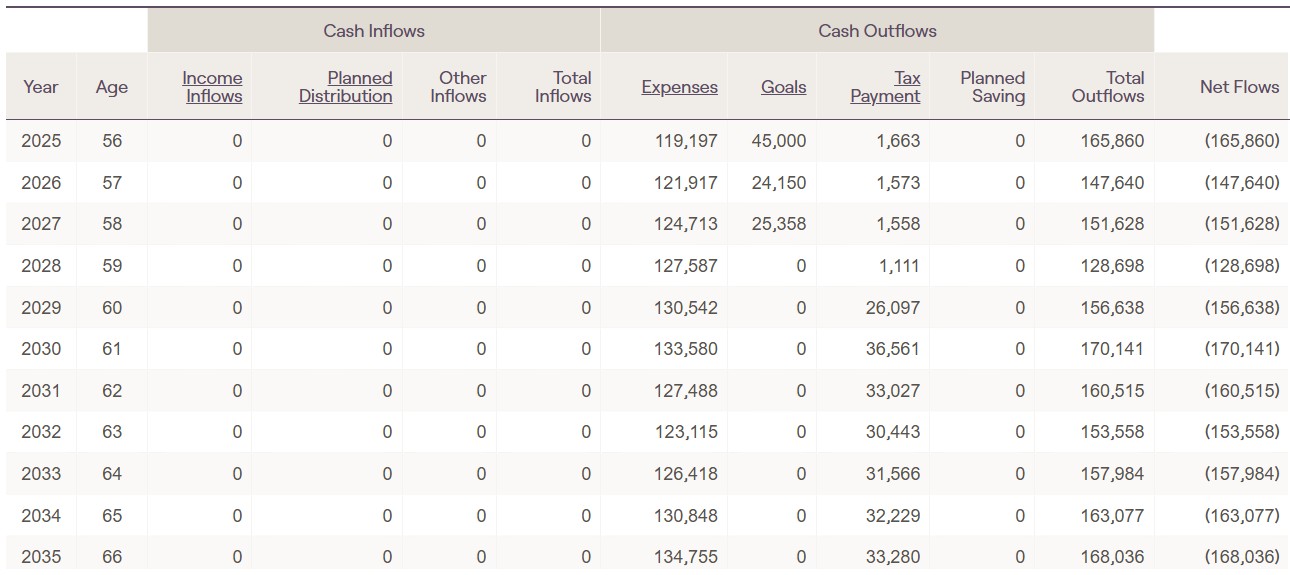

Summary of Cash Flows

The $8,000 that she wants to spend per month is going to be after tax money. So, that will be $96,000 of living expenses annually. Plus she has housing, which includes paying down her mortgage.

Again, she has a very low mortgage rate under 3%, so we're not worried about her getting that paid off right now. She could pay that off at any time because she has the funds to do it. But again, a low mortgage rate, so it's not a huge concern.

On top of her living expenses, she has education goals. She's got a little bit under $100,000 left to pay for Phoebe 2 and Chandler Jr. So that will be taken care in a couple of years.

If we look at income flows, she's got no more income because she's going to be retired. So her net flows is how much she's going to have to take from her investments to live the way that she lives, spending the $8,000 per month.

The expenses are inflation adjusted by 2.5% because, obviously, we're going to have inflation of some sort. We don't know what it's going to be, but I still feel like between 2 and 3% is probably a good estimate long term, even though that is often in flux. We can always change those numbers if you like.

Then she will have income from Social Security starting at age 67 and RMDs starting at age 75.

Remember that the goal is to basically get a map for you so you have a good starting point of where you're going to be because right when you walk out the door, things are going to start to change.

That's why it's good to always walk with someone for your situation because the goals and the plan of what you're going to need is going to change certainly over a 30 or 40+ year retirement.

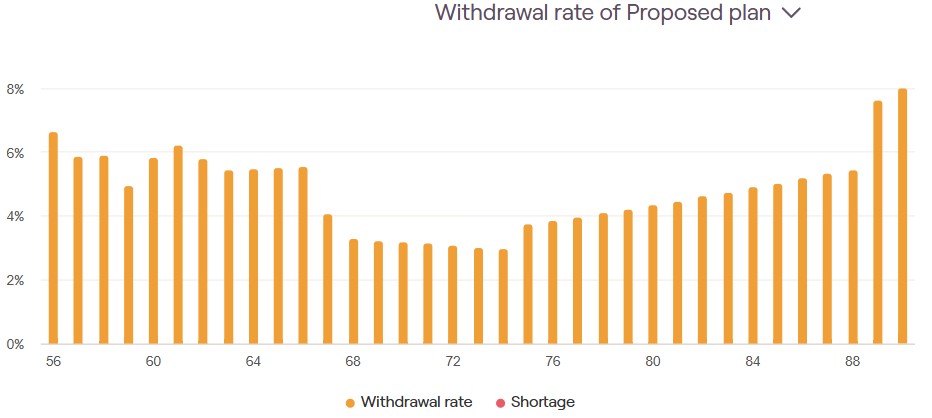

Withdrawal Rate

Let's also take a look at Monica's withdrawal rate and see if this is going to work for her. We always want to look at the withdrawal rate and make sure that what she is spending and what she has coming in are sustainable throughout her retirement.

I run these plans to age 90. Obviously, once people get in their 80s and get closer to that age, then we can make adjustments from there. Or if something comes up, God forbid, earlier, we can make those adjustments, as well.

Being relatively young at age 56, we're going to just run it to age 90. If we start looking, 6.6% is on the higher end of a withdrawal rate that I would want to do. But it's only for a few years, then we drop back down to about 4 or 5%. Then we see once Social Security kicks in at age 67, it drops down to 4%, then 3%, and then it starts ticking back up as she ages.

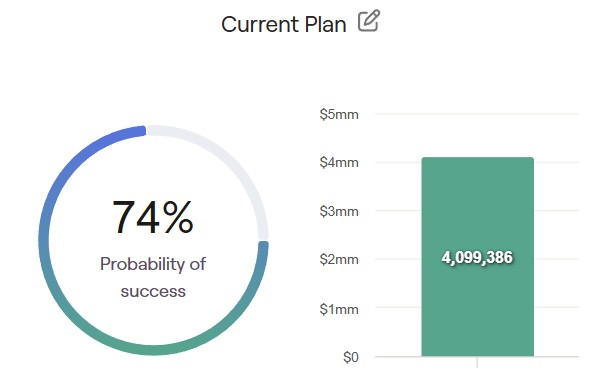

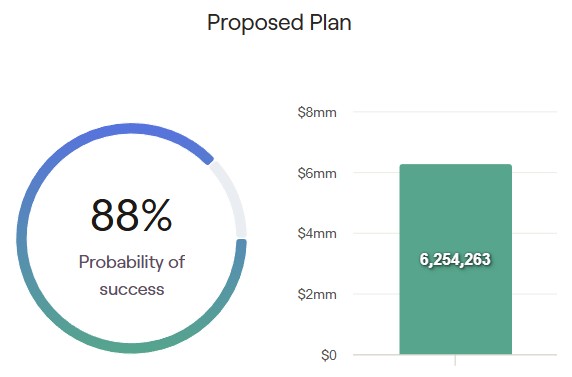

This is run through thousands of Monte Carlo simulations. If she does nothing, it's showing that at age 90 she's going to have about $8.6 million at the end of her plan. This is if she changes nothing and keeps spending the $8,000 per month as she is right now. So that's a pretty good situation!

Probability of Success

If we look at a percentage, it shows a 74% probability of success. Now, this is a little bit misleading, but basically what that means is there's a 26% chance that we're going to have to make changes, which we're always going to make changes anyway.

Sometimes people say, "I want you to increase that up to 90%" or whatever. But then if you're at 100%, that's basically a 100% chance that you are not going to spend enough in your retirement.

Some people live the way they want and they're at 100% and they're comfortable with that. But I always like to let people know they have choices. At a 100% probability, you might as well do something to try to maximize your life in retirement.

Retirement smile

Let's take a look at a few changes. In retirement, you'll have expenditures. Certainly, if you retire younger, you'll probably spend more early on in retirement, maybe hang out with your family, maybe go traveling, doing whatever.

That situation is called the Smile retirement spending strategy, which means that you're going to spend a little bit more upfront and then probably have a little lull until you get to the end of life in which your healthcare costs go up. So, if we adjust Monica's settings to do the smile spending strategy, then she has an 88% probability of success.

Now, again, this is a 12% chance, which is a lot lower than 26% chance, of having to make some changes. We do like this strategy because it's very standard right now.

I see that even with my own family, you know, relatively healthy and getting around well, they've done a lot. They get to this point where they want to start slowing down a bit when they get to their 70s or so. They're still going to do what they want, but they don't need to do all the stuff that they used to do. They don't have the desire to do that anymore. They just want to see their family and have a good time. That is pretty standard.

For Monica, this is a perfectly good situation. So, yes, she could retire today and have a very good probability of success in her retirement.

Increasing spending

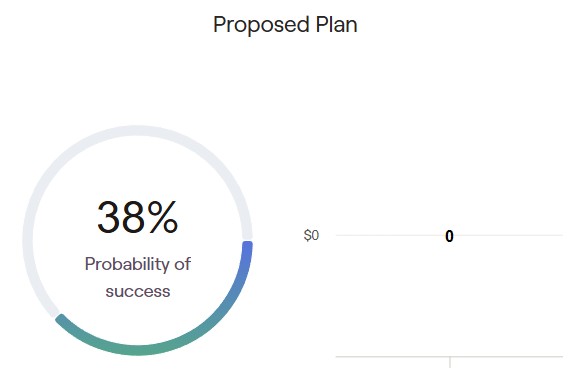

Let's say she wants to increase her spending to $10,000 per month instead of $8,000. That drops her probability of success down to 38%. So, that's going to make things a little tighter.

And it shows still shows at the end of her plan (in green below) at age 90, she's going to have about $1.4 million of investable assets, but we're not sure how that's going to work out.

Tax Strategy and Potential Savings

Another big thing that we do at my firm is tax planning. A big goal in retirement is to make sure that we are limiting lifetime tax liability. Usually our largest expense in retirement is taxes.

I can almost guarantee from everything that I've seen, people that don't plan to manage their lifetime tax liability are going to end up spending more.

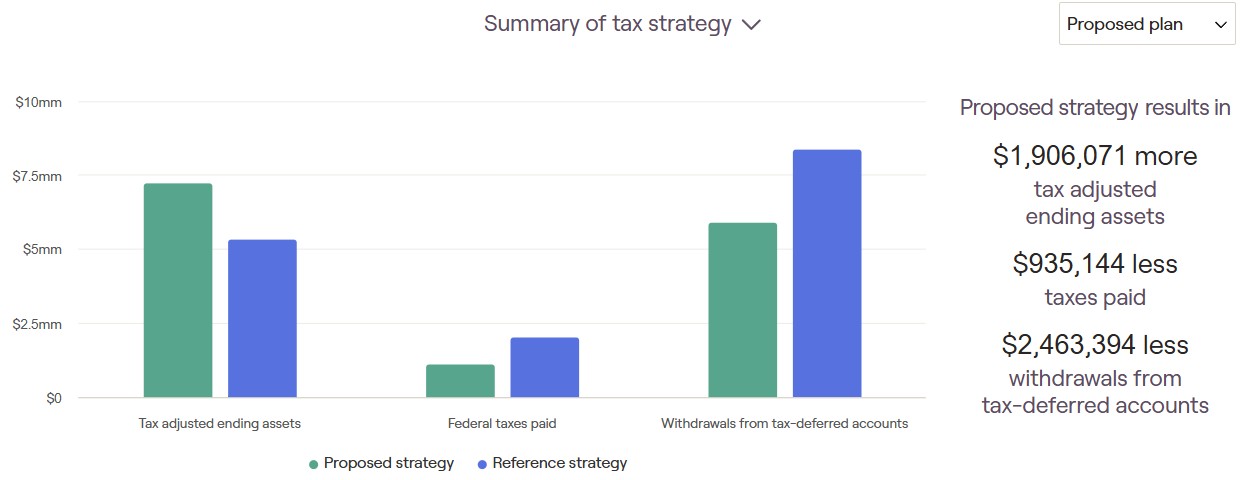

But let's take a quick look at Monica's tax strategy. We put everything back to the way it was at the beginning. She's going to have about $1.9 million more in tax adjusted ending assets. So, not chump change, right? And pay almost a million dollars less in taxes.

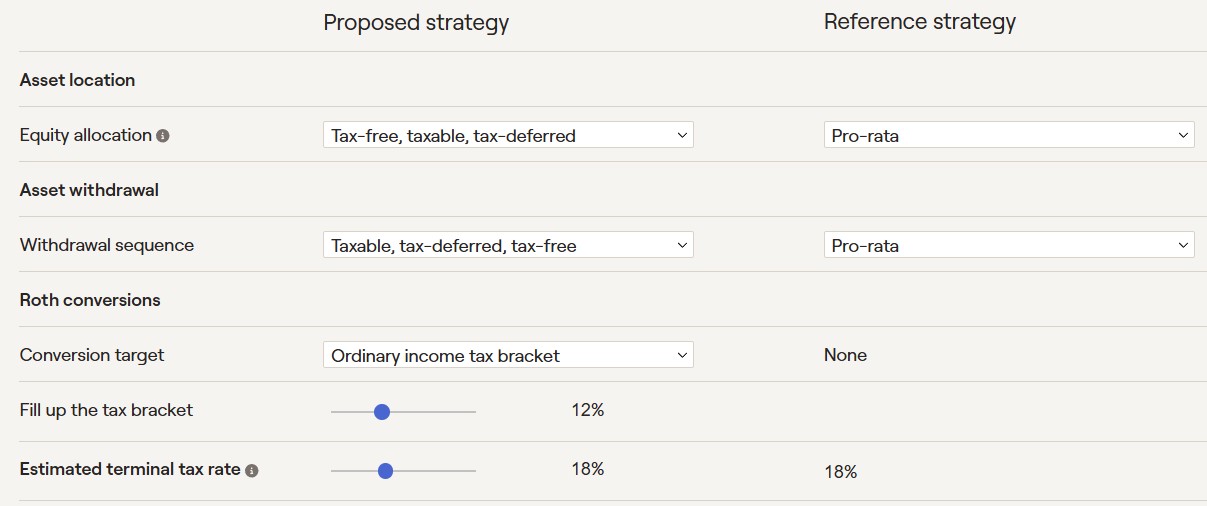

Now, how does that happen? The three big things that we're going to do is:

- Roth conversions

- Equity allocation

- Sequence of withdrawals

Roth conversions

I've already run the numbers and the software is simulating converting up to about the 12% tax bracket, which is a little tight because she's going to be filing individually, but she's still not going to have any income.

That gives us a few years where we can do some decent-sized Roth conversions until Social Security kicks in at age 67 for her. Every single year, we're going to look at her taxable situation and we're going to thread that needle with limiting lifetime tax liability.

Equity allocation

Equity allocation basically means if you have growth investments, you want to put those in a Roth or even a taxable account because you're going to have a better tax status.

If we have something go from $10 to $100 over time. You want to let that be in a Roth because you're not going to pay any tax on it when it comes out.

You don't want the growth asset be in your tax deferred account because if it goes from $10 to $100, you're going to have to pay tax on that $100, and you're going to be in the seven bracket ordinary income rates.

Sequence of withdrawal

Where you take your money from in retirement can really have a large impact on your income for that year and subsequent years, and certainly it can make a very large impact over the lifetime of your retirement.

By doing these three things: (1) converting the proper amount of into a Roth IRA each year to mitigate your lifetime tax liability over time, (2) making sure that we're doing equity allocation right, and (3) doing sequence of withdrawal correctly, it's going to add almost $2 million of tax adjusted ending assets to Monica's portfolio.

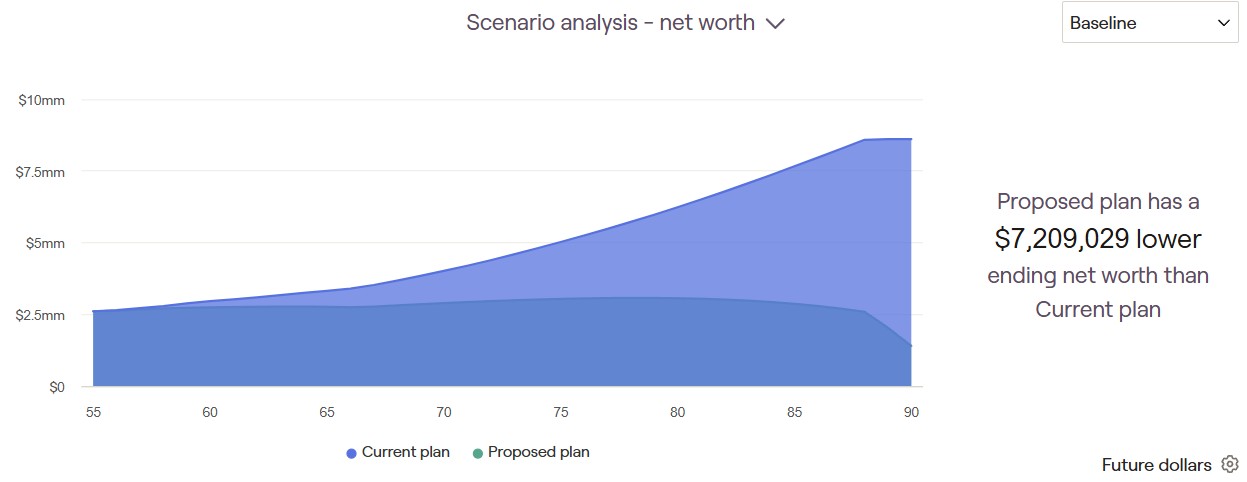

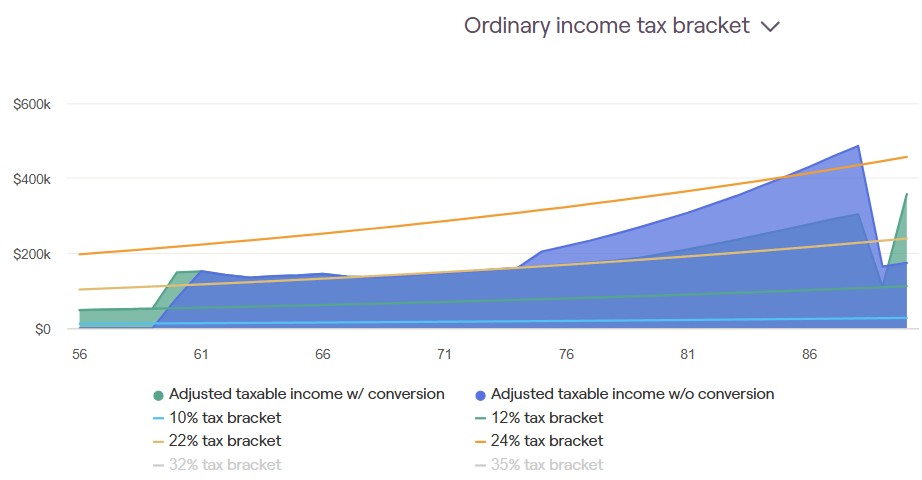

Let's take a look at a visual of that. The blue represents if we did nothing. We didn't pay attention to where we were taking money. We just take the same amount from each account. We didn't do any Roth conversions, so we're going to have all this lifetime tax liability.

However, the green represents if we do all three things that I discussed, it's going to flatten that curve, and we're going to alleviate all this tax that she would have to start paying more on at age 75.

Why is that? Well, if you let your tax deferred accounts keep growing the way they are, your RMDs are going to be higher and higher, and that's going to cause you to step up in the seven bracket ordinary income tax brackets.

We don't want to do that when we can mitigate this, right? If we can convert some assets now, in these gap years between retirement and when RMDs kick in, we're going to flatten that retirement tax amount.

It's also going to prevent increases in your parts B and D Medicare premiums. Those are based off your AGI, your adjusted gross income.

One time I had a guy say, "Oh, Tim, I won't care about taxes in my 70s or 80s. I'll just be happy to be there.

Well, let me tell you what. I have clients in their 80s and 90s and they still don't like a large tax bill. And some of them didn't do these strategies back, you know, 10, 20 years ago. So now they have to pay really high amounts and their parts B and D Medicare premiums their tax rates are a lot higher than they had to be had they done the proper planning at the time.

Going Further

If you are interested in seeing other case studies, check out the videos in these posts:

- We Have $3.5 million, Can We Retire and Maintain Our Lifestyle?

- Can We Spend $10,000 per Month in Retirement?

- We have a $2.4 Million Portfolio; Can I Retire Tomorrow and Continue Our Same Lifestyle?

- How Much Can We Spend if We Retire Tomorrow?

- How Much Can I Save in Taxes with Roth Conversions?

- How Much Can I Spend in Retirement from a $1 Million Portfolio?

- Is $1 Million Enough to Retire at 65?

- Real Life Case Study Saving Over $1.7m in Retirement Taxes

A CERTIFIED financial planner™ professional can help you plan for your retirement. Schedule a call today so we can talk about your situation.